Why the RMB is depreciating?

2016-01-07 贝乐斯 (作者) Bei Le-si (Author), Dimensions Capital Management

China Tax & Investment Consultants Ltd expresses great gratitude to the author for his permission to reproduce the Chinese version of this article.

今年以来仅三个交易日,离岸美元兑人民币汇率就升值2.35%,已经超过二年期人民币定期存款的利息。去年8月10日到今天,美元兑人民币的在岸汇率升值5.6%,而同期上证指数则下跌10%。人民币贬值趋势已经非常明显。人民币为什么会贬值?

Only three trading days into the year of 2016, the dollar in the offshore market has already appreciated against the yuan by 2.35%, exceeding the interest earned from 2-year RMB time deposit. Since 10th August 2015, onshore US-yuan exchange rate has gone up by 5.6%, while the Shanghai Stock Exchange Composite Index has fallen by 10% during the same period. The trend for a sustained yuan weakness is obvious. What is the reason behind the yuan depreciation?

想要搞明白为什么人民币会贬值,就要先搞清楚过去这十几年人民币为什么持续升值。过去这些年,中国经济快速发展,到处都是投资的机会,海外资金大量流入,推升人民币汇率。另一方面,中国成为了世界工厂,出口快速增长,顺差越来越多,也推升了人民币汇率。而从2009年开始,一个不为人知的重要因素则支撑了人民币汇率的上涨,目前也是这个因素决定了人民币汇率贬值是一个极为确定的事件。

Before getting to know why the yuan has depreciated, it is imperative to know the continuous hike of the yuan against the dollar over the last decade-plus. During that period of time, huge amount of foreign capital poured into China as the Chinese economy grew at a very fast rate and investment opportunity was abundant, which pushed up the yuan exchange rate. On the other hand, China became the world factory with rapid increase in exports and surplus in the trade balance, thus pushing up the yuan exchange rate. Beginning from 2009, however, an important factor unknown to the market bolstered the hike in the yuan exchange rate, and it is also this factor that makes the depreciation of the yuan a certainty.

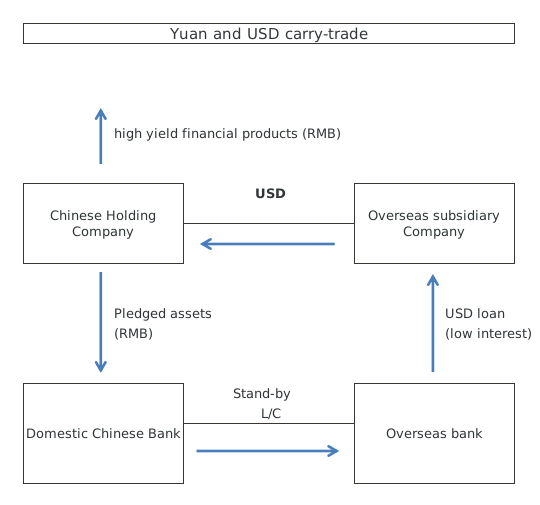

几年前,我在读某造船企业的年报时发现了明显的异常。这个公司的理财投资占了60%以上的利润,已经超过了造船主业。资产负债表上价值高达百亿人民币的大量境内理财信托投资靠的是大量境外美元贷款支撑。企业在国内抵押人民币资产,向银行获得全额的美元信用证额度,相当于获得了金融杠杆。企业的海外子公司凭借母公司在国内银行开出的美元信用证担保,从境外银行获得短期美元贸易贷款。然后境外子公司把获得的美元资金以各种方式汇入国内,提供给母公司在国内投资获利(有杆杠的理财产品或者房产)。

A few years ago, the author found an anomaly in the annual report of a ship-building company. The income earned from the investment in financial products accounted for over 60% of the total profit, exceeding the income derived from the principal ship-building business. As shown in the balance sheet, the USD loan arranged from outside China became the major source of funds for the investment in various trust-type financial products amounting to 10 billion yuan. This company obtained USD L/C facilities from the bank and the resulting financial leverage, by pledging the yuan assets it owned in China. The foreign subsidiary of the parent company obtained short-term USD loans from the bank, on the strength of the stand-by letters of credit issued by the banker of the parent company in China. And then, the foreign subsidiary channeled the USD back to the parent company through various means of inward remittance, so that the parent could profit from the investment in the higher yield financial products.

半年期美元贸易贷款利息大约3%,而如果汇入国内,投资于理财信托产品,则有10%的回报,再加上人民币兑美元的升值,再乘以杠杆,企业的收益是(7%+人民币升值)x 杠杆率。即使是保守的两倍杠杆,由于人民币在2010年到2013年每年升值1.4-5.0%左右,这个公司的回报率至少在20%以上。这样的回报率,在实业越来越艰难的时候非常可观。难怪这个公司的老总认为这是一个低风险,高回报的新业务,大力拓展。这些做实业的企业家,不懂金融,更不懂金融的风险,却首先尝到了金融杠杆套利的甜头。一旦尝到了血的味道,实业领域辛辛苦苦打拼挣钱的一点儿利润早就看不上眼了。

During that period the interest rate for trade financing of 6-month duration was about 3% while the return on investment in the trust-type financial products gave 10%. Coupled with the Yuan-USD appreciation and the built-in leverage in those financial products, the yield for the enterprises would amount to the following sum: (7% + yuan appreciation + leverage). Given the least conservative leverage of 200%, the return to the enterprise will be no less than 20% per year, due to the 1.4% to 5% appreciation of the yuan from 2010 to 2013. The 20% return on investment was pretty much attractive at a time when running the core ship-building business faced with escalating difficulty. It is no wonder that the CEO of the enterprise would consider the currency carry-trade is low-risk, high-yield business, and made great effort on the carry-trade. The entrepreneur who possessed the skills to do manufacturing business but no knowledge of the financial products and the operations in the financial market, started to profit from the carry-trade in the currency market for the first time. Once they had a taste for it, they would place a low priority on the small profits that they worked hard to earn from the manufacturing business.

这还只是一个企业而已。我查了查国际清算银行的统计,这种套利的资金竟然高达一万多亿美元。更为危险的是,这一万多亿套利资金,有高达70%是一年以内的短期贷款,必须不断的滚动续借。

That is only a drop in the ocean. The author found from the statistics compiled by the Bank of International Settlements that this type of carry-trade amounted to as much as one trillion US dollar. The more risky things are that 70% of these one trillion US carry-trade funds are financed by short-term loans, which must be redeemed on a rollover basis continuously.

一万多亿美元不是小数目,大约占外储的三分之一。也就是说外储里约有三分之一是套利热钱,一有风吹草动,不得不走。现在实体经济回报越来越低,外资不再大量流入,仅仅靠顺差已经无法抵消资本外流的压力,人民币汇率开始贬值。这一万多亿美元的套利资金面临着灭顶之灾。首先,由于美联储升息,海外美元贷款利息上涨。其次,国内投资理财的回报率越来越低。最关键的是人民币贬值让套利空间反转,变为加杠杆亏损。这样一来套利的大趋势已经反转,套利者必须逃离。这种情形在不久前的A股也上演过。投机者大肆用融资配资高杠杆,推高股市,获得几倍的高回报,却在股市下跌中集体踩踏出逃。

One trillion US dollar is no small amount. That accounts for about 1/3 of China’s foreign exchange reserves. In other words, one third of the reserves are hot money for the carry-trade. They will leave China when the situation does not look good. At the moment, the return from real economy is getting lower and lower. Without large amounts of inflow foreign capital, it is difficult for China to offset the amount of capital outflow by the inflow arising from the surplus in the trade balances, and thus the yuan will start to depreciate against the dollar. This one trillion US engaged in the carry-trade is heading for disasters. First, the interest rate for offshore USD financing will rise in the wake of the rate hike announced by the Federal Reserves. Second, the rate of return from the financial products in the domestic market is getting lower and lower. The crux of the issue here is that yuan depreciation has reversed the yuan-USD carry-trade, turning profits into huge losses due to the accelerating effect in the leverage. The table for the carry-trade has turned, the carry traders must flee. The same has happened in the A-share stock market. The speculators trading on high margin financing pushed up the stock market index, and earned high returns of several times. But they were all caught in the stampede during the stock market crash.

如果趋势反转能缓慢有序进行,投机套利资金逐渐退出,人民币贬值的压力也许还小些。但是,金融市场的规律就是一窝蜂。在《金融炼金术》一书中,索罗斯写到“而更重要的则是,当一个趋势的改变被大家识别出来,投机交易的量有可能经历大规模,甚至是灾难性的增加。当一个趋势持续起来时,投机流动是逐渐增加的。但反向的变化不仅涉及目前的流动,还涉及到积累起来的存量投机资本。趋势持续的时间越长,积累的存量越大。当然,也有一些缓和的情况。一个就是市场参与者可能只是逐渐认识到趋势的改变。另一个就是当局肯定会意识到危险从而采取行动来避免崩溃。”目前看,套利者早已经认识到了趋势的改变,而央行在做了各种努力之后已经没有意愿,也没有能力,在目前的汇率水平保持人民币汇率的稳定。

Should the currency carry-trade reverse in an orderly manner and the arbitrage capital flow out of China gradually, the pressure for yuan depreciation will be less. However, the order of the financial market is like a swarm of bees. In his book “the Alchemy of finance”, George Soros writes: “more important is when a trend of change is recognized, the volume of speculative transactions is likely to undergo a drastic, not to say catastrophic, increase. When a trend persists, the speculative flows are incremental; but a reversal not only involves the current flows but also the accumulated stock of the capital. The longer the trend has persisted, the larger the accumulation. Of course, there are mitigating circumstances. One is that the participants of the market are likely to recognize a change in trend only gradually. The other is the authorities are bound to be aware of the danger and do something to prevent a crash.” For now, the carry traders already spot the change in trend, while the central bank, after trying to turn things around on various occasions, has lost the willingness and the ability to keep the exchange rate of the yuan to stabilize at the current level.

什么是真正确定性的机会?当市场参与者身不由己,不得不做的时候,就是真正确定性的机会。索罗斯说的反身性就是这种情况。泡沫中,参与者身不由己,不参与就会损失赚大钱的机会,你不参与别人也会参与。泡沫破裂,你不跑,别人会跑,不跑你就会被踩踏致死。目前的人民币汇率,你不换,别人会换,想想后面还有一万多亿美元的套利资金需要换汇,现在的价格真的很优惠了。这些套利资金,面临着灭顶之灾,必须换美元,属于“亡命之钱”。而海外银行不是慈善家,总会在下雨时收回雨伞,收回美元贷款。这样一来,未来几年人民币贬值的趋势就很明显了。

What is the real and certain opportunity? It is when the market participants find that they must do it. That is the real and certain opportunity. Soros said reflexivity is such a situation. In the bubbles, the participants cannot help do it. They will lose if they do not participate in it as others will participate. When the bubble bursts, others will run if you do not run. If you don’t, you will be dead in the stampede. At this level of the US-yuan exchange rate, other will do the conversion if you do not do. Thinking about the one trillion US carry-trade money, the yuan price for now is very attractive. These amounts of carry-trade money are in for disasters. It is a life or death situation and the money must be converted into the dollar. Bankers outside China are no philanthropists. They will always call back the USD loans when credit conditions are tightened. It goes without saying that the trend for a weakening yuan in the next few years is too obvious.

人民币为什么会贬值?除了经济因素,最重要的是高达一万多亿美元套利资金的反转。投机者在前几年享受了盛宴,加杠杆轻松获得了高额的收益,推高了人民币汇率。如今,投机者仓皇而逃,让人民币贬值,却让全体持有人民币资产的人买单。

Why the yuan is depreciating? In addition to the economic factors, the most important thing is the unwinding of the USD carry-trade that amounts to as much as one trillion US plus. The speculators have enjoyed the feasts during the past years, and got high returns using the financial leverage, pushing up the exchange rate of the yuan. For now, they are fleeing China, leaving those who hold yuan assets to foot the bill for the depreciated yuan.

China Tax & Investment Consultants Ltd Copyright 2000-2025. All rights reserved. Notice of Copyright and Disclaimer